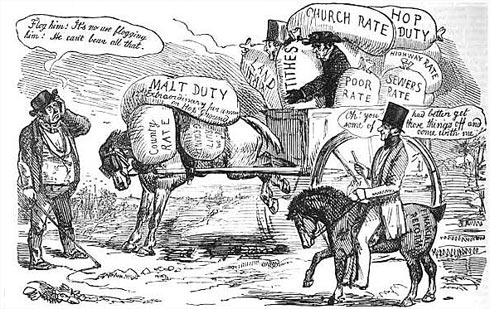

Today is tax day in the U.S. I paid mine in March. My tax receipts are sometimes 5 inches deep in paper. As a self-employed author and retired teacher, I save receipts for lodging, mileage, advertising, home office, technology, insurance benefits, medical expenses, etc. But what were some of the taxes required in the Regency Period and when would they pay their taxes?

We know there were taxes upon hair powder, carriages and coaches, and carriage and saddle horses, windows, and male servants during the Regency.

In 1777, Lord North proposed a tax on male servants to help pay for the cost of fighting the Americans, and by 1808, when Britain was involved in an even more prolonged war against the French, the tax reached a little over £7 per year for each male servant if there were eleven or more in the household. For the servants’ tax, an estate owner would pay for those who performed non-essential services: “butlers, footmen, valets, grooms, coachmen, gardeners, park-keepers, game-keepers, masters-of-the-horse, whippers-in and other huntsmen, were all to be taxed. But farm laborers, day laborers, factory workers and the servants of tavern-keepers, shop-keepers and merchants were all to be exempted from the tax. So, too, were the servants of the royal family, official foreign ambassadors and the servants in the various Colleges. However, if an inn-keeper, shop-keeper or farmer were to employ one of their servants to perform personal or domestic services, such as scrubbing a floor, saddling a horse or cleaning boots, their masters would then be expected to pay the tax on that servant. Few would voluntarily pay the tax, but had to be careful about when and where their servants performed those prohibited tasks, as there was always the chance a rival or adversary might inform against them.” (Regency Redingcote) In 1843, the Earl of Ashburnham paid taxes for the half-year of £21 15s 9d for his male servants, another £11 for his four-wheeled carriages, and £1 4s for armorial bearings, plus a ten percent surcharge. (MS Ashburnham. 1814. East Sussex Record Office)

From 1785 – 1792, a tax was also levied on those employing female servants at the rate of one guinea on each one. This tax had nasty effects on the labour market and only lasted for seven years before it was repealed.

King William III levied a window tax beginning in 1696. The tax was to level the difference resulting from the clipping and defacing of silver coins, as well as to help pay for the various wars in Ireland and Europe. Initially, if a household had less than 10 windows, they were charged 2 shillings per year. 10-20 windows would cost 4 shillings. Those houses with over 20 would be 8 shillings. The window tax increased 6 times between 1747 – 1808, before a decrease came about.

King William III levied a window tax beginning in 1696. The tax was to level the difference resulting from the clipping and defacing of silver coins, as well as to help pay for the various wars in Ireland and Europe. Initially, if a household had less than 10 windows, they were charged 2 shillings per year. 10-20 windows would cost 4 shillings. Those houses with over 20 would be 8 shillings. The window tax increased 6 times between 1747 – 1808, before a decrease came about.

The Glass Excise tax was in existence for 100 years. It was first levied by Parliament in 1745. Taxes were levied upon window and bottle glass, as well as flint glass. (With respect to glass, the term flint derives from the flint nodules found in the chalk deposits of southeast England that were used as a source of high purity silica by George Ravenscroft, c. 1662, to produce a potash lead glass that was the precursor to English lead crystal.) Initially, the tax was purely on materials, with flint and white glass, crown and plate charged at the highest rates. Green and other bottle glass was charged at a lower rates.

For 90 years, beginning in 1784, people paid taxes on pleasure horses (race horses, those let to hire or rode by bailiffs or butchers, horses exceeding 12 hands (height), but not work horses.

Charges varied for Horses for riding (£1.8s.9d). In 1785 an Act exempted those occupying a farm worth not more than £150 a year rent in which the horse was used only for riding to church or market. The yearly exemption rate was reduced to £20 in 1802 and thus many more owners were taxable.

An Abstract of the Principal Tax Acts from 1819’s Gentleman’s Pocket Memorandum Book, tells us that a man with one carriage would pay £12 per year in taxes. Two carriages would be £26, etc. Carriages drawn by one horse with less than 4 wheels (Taxed carts excepted) 6£ 10s if drawn by 2 or more horses, 9£ and every additional body used on the same carriage, 3£ 3s. Dog lovers who kept greyhounds, whether his property or not, would pay £1. For every other species of dog, where more than one is kept, 14s. Every person wears hair powder would pay 1£ 3s 6 d.

From 1695 to 1706, a “marriage tax” was assessed on bachelors, widowers, and childless couples. It was also charged for parish register entries of baptism, marriage, and burial.

Beginning in 1793, those who had an armorial bearing marking carriages, etc. paid two guineas for arms borne on carriages and one guinea if borne in any other way, as on a signet ring. This lasted until 1882.

From 1795 to 1861, those who used hair powder, (to keep wigs white), had to pay a guinea to £1.3.6 for a licence to do so. The tax included those servants required to wear wigs. Exemptions included the royal family and their immediate servants, army officers, clergymen, dissenting ministers, and any person in holy orders not possessing an annual income of £100. Wigs quickly went out of fashion in the early 19th century, although the tax was not abolished until 1861.

How long before a tax lien would be placed on the property? The delinquent tax payer would be taken before the judges of the court of the Exchequer to have the debt filed formally and the order for property to be seized. The property of peers was handled different from that of commoners, though it was still seized. Theoretically, if a man’s taxes were delinquent in a particular calendar year, he would not be formally labeled as delinquent until after April 6 of the next calendar year. Attempts would then be made to collect the back taxes before seizure of the property would be made. More than likely it would take two, perhaps three, years for the seizure to take place. Meanwhile more taxes would be accumulating while the courts acted.

Again, however, it really depends on what taxes and to whom they were due and how they were paid. Needless to say if a duke owed taxes, he would be treated differently than a merchant.

An unwelcome visit Woodward del. http://blog.americanduchess.com/2012/02/v33-only-death-and-taxes-in-18th.html

There were hundreds of taxes and so a variety of dates on which they would be due. Some taxes were pay as you go. For others, the tax man came along and counted your windows and looked at your footmen and counted the crested carriages and other armorial bearings and wheeled vehicles and made his demand. A person then had a stated amount of time to pay the tax. Some taxes were due on quarter days and some on cross quarter days. The quarter days were four dates in each year on which servants were hired, school terms started, and rents were due. They fell on four religious festivals, roughly three months apart. Leasehold payments and rents for land and premises in England are often still due on the old English quarter days. The quarter days ensured that debts and unresolved lawsuits were not allowed to linger on. Accounts had to be settled, a reckoning had to be made and publicly recorded on the quarter days.

The taxes were due in quarterly installments until the late 1800’s, and tax day was changed to 6 April in 1800.

In typical style, the Treasury ensured that there would be no loss of tax revenue and no concession to the populous by making the tax year 365 days. To complicate the matter, we have the New Style Calendar. The Calendar (New Style) Act 1750 was an Act of the Parliament of Great Britain. It reformed the calendar of England and British Dominions so that the new legal year began on 1 January rather than 25 March (Lady Day); and it adopted the Gregorian calendar, as already used in most of western Europe.

In England and Wales, the legal year 1751 was a short year of 282 days, running from 25 March to 31 December. 1752 began on 1 January. To align the calendar in use in England to that on the continent, the Gregorian calendar was adopted: and the calendar was advanced by 11 days: Wednesday 2 September 1752 was followed by Thursday 14 September 1752. The year 1752 was thus a short year (355 days) as well.

In England and Wales, the legal year 1751 was a short year of 282 days, running from 25 March to 31 December. 1752 began on 1 January. To align the calendar in use in England to that on the continent, the Gregorian calendar was adopted: and the calendar was advanced by 11 days: Wednesday 2 September 1752 was followed by Thursday 14 September 1752. The year 1752 was thus a short year (355 days) as well.

Several theories have been proposed for the odd beginning of the British tax year on 6 April. One is that from 1753 until 1799, the tax year began on 5 April, which corresponded to 25 March Old Style. After the twelfth skipped Julian leap day in 1800, it was changed to 6 April, which still corresponded to 25 March Old Style. And so the 1800 tax year was moved from 25 March to 5 April. Having done it once, the Treasury then decreed in 1800 that there would be another lost day of revenue, given that the century end would have been a leap year under the Julian calendar whereas it was not under the new Gregorian calendar. Thus 1800 was a leap year for tax purposes, but not for the purpose of the calendar and so the tax year start was moved on again by a single day to 6 April. However Poole thought that quarter days, such as Lady Day on 25 March, marked the end of the quarters of the financial year.] Thus, although 25 March Old Style marked the beginning of the civil year, the next day, 26 March Old Style was until 1752 the beginning of the tax year. After removing eleven days in 1752, this corresponded to 6 April New Style, where it remains today.

One has to be certain that the income tax was in force during the year in question and that it was a tax due on the 6th and not on some other day.

For more information check out these sources:

Regina, this was particularly interesting for me because I worked for HM Revenue and Customs (the Inland Revenue in the days I worked there) from 1967 to 1990.

Carol, you are like me in so many ways. I worked for a tax preparer for some 10 years. I did learn something from your response. I did not not know the term “Inland Revenue.”

Regina, even after I left the Inland Revenue, I still worked in tax, but in the tax departments of various accountants completing Tax Returns for clients and other related work. Now, when anyone talks about the UK Inland Revenue, you will know exactly what they mean, although nowadays it would be HM Revenue and Customs.

Carol, I keep a master file of tidbits such as this one so if I have questions, I can look things up there instead of spending hours on the internet.

As another self-employed person, I’m also snowed under with receipts that I have to keep! As we’ve recently passed the end of the Tax Year over here, I’m now in the process of collating everything in preparation for filing my Tax Return. Fortunately, I don’t have any horses, carriages, servants or wigs to declare! Interesting to note that having a coat of arms on a carriage or even a signet ring attracted an extra amount in tax, so that really was showing off that you’d got plenty of money.

I’m glad you’ve mentioned that bit about taxes on horses being used for pleasure purposes. It came up in a discussion on another blog recently and although I was sure I’d definitely read about it somewhere, I couldn’t reference the source at the time. I may just go back there and add a link to your post here.

Thanks, as always, for an extremely interesting article.

Monday, the 18th, is tax day here in the U.S., Anji. It is supposed to be the 15th, but with Easter and all, for a second year, it was moved to the 18th. Nancy Regency Researcher (mentioned above) has a nice piece that speaks to horses, mules, etc.

As usual, Regina, you’ve used your amazing research abilities to bring us a most readable and informative article. It would seem, unless I missed something, the only thing missing was the application of a tad bracket. Tax brackets, as applied here, have given rise to credits, progressive and regressive taxes, etc. Given the complexity of our tax code today, I think I might be a tad happier with England’s system “back then”. I doubt I’d be too thrilled with what I hear of their system today any more than our system here. Thank you for today’s education!

For many years, I worked as a tax preparer, but I would not want such a job now. Although I am very mathematically inclined, I thought the course was tough then.

Great article Regina ……I love all the interesting collection of info. you have from this period … one of the many reasons why I enjoy period Romance … the historical information is very enlightening and funny, but I suppose our modern ways would be even funnier. However, I see I am going to have to cut back on my use of HAIR POWDER as the price is too steep …. will have to use flour instead …. hope it doesn’t rain!!..lol Thank you again for the share ….. Judith

And I must remove the Jeffers’s insignia from the side of my Buick Lacrosse. LOL!